Impact Investing is changing the way investors value companies. It’s a new way to view financial markets, and it has huge potential to change the world for the better.

In basic terms, impact investment involves investing in companies that are having a positive social or environmental impact on the world. In a world where government’s seem unable, or unwilling, to regulate carbon emissions, or combat inequality, it’s being left to investors to drive change.

While it may sound simple, it’s a radical concept. Investors are now requiring companies to report more than just their financial results—they’re asking them to report their social and environmental impact as well, both positive and negative.

This is Part 1 of the Future of Investing series, stay tuned.

Since the term was coined in 2007, the field of impact investment has grown rapidly.

It’s gone from being a niche investment strategy, focussing on private equity funding, to spanning most asset classes and offering impressive returns.

The Global Impact Investment Network (GIIN) is the leading body bringing together the leaders in the space, and their definition of ‘Impact Investing’ is the most widely used:

“Impact investments are investments made with the intention to generate positive, measurable social and environmental impact alongside a financial return.”

It’s a succinct description, but still, the term is widely misunderstood.

In this article I’m going deeper, I’ll explore:

The Origins of Impact Investing

The term impact investing was coined by a group of concerned investors who were brought together by the Rockefeller Foundation in Bellagio, Italy, in 2007.

The group recognised the immense power embedded in the capital markets, and they wanted to direct it to have a positive impact.

They were frustrated, that the businesses doing the most good in the world often couldn’t get capital. While those damaging the environment, or exploiting society, didn’t have to pay for the negative impacts (the negative externalities) they had on the world.

Impact investing was a new way of identifying businesses that would be both financially successful, while also helping to solve some of our world’s most wicked problems.

They foresaw that the most sustainable and transparent companies would offer better long-term performance.

Many of the attendees of the meeting would go on to be leaders in the field.

And early pioneers like Jed Emerson, Cathy Clarke and Antony Bugg Levine are having a major influence today.

The long history of socially responsible investing

While the modern iteration of ‘impact investing’ was coined at the meeting in Bellagio, the concept of applying an ethical or values-based filter to your investment decisions is much older.

The concept has been operating in the United States for over 100 years, since the Quakers Friends Fiduciary Corporation put a restriction on investing their funds in weapons, alcohol and tobacco in 1898.

And there are claims that even the Dutch merchants of the 17th century made ethical distinctions about whether their ships could be used to transport troops to fight wars, as well as their regular merchandise trade.

In the modern era, in the 1960s to 1980’s, we saw a protest movement against apartheid in South Africa being led by calls for universities and companies to divest from South African companies. More than 200 US companies, as well as UN bodies, sold their stakes in businesses in South Africa.

While divestment is distinct from impact investing, these actions highlight the long history of using investment decisions to create positive change in the world.

Impact investing has its roots in private equity

In the early days, impact investing followed the private equity model where investment firms or family offices would invest directly in a private company (this is a company that’s not listed on a stock exchange).

The investor would identify a company in which they could take a controlling share, and where they could offer management assistance and expertise to help the company grow. The aim was to boost the company’s positive impact, as well as its profits—and they stayed close to the management of the business.

In-line with the private equity model, these investors would eventually want to sell the business, to realise a financial gain. With the hope that the positive impact could then be ‘scaled-up’.

This is the evolution of impact investing where the inherent social and environmental impacts of small, local businesses is multiplied and expanded to serve a wider market, and produce ever-more impact.

In the process it’s also proven that companies don’t have to follow the industrial-era model of extractive capitalism to be successful and profitable.

It’s built a model for sustainable business, that considers local communities, and the environment, as much as gaining market share.

This model has proven so successful that it’s pushed beyond the bounds of private equity to influence all the major asset classes; from listed equities, to fixed income, green-bonds and property investing.

For more Impact-Insights, sign-up

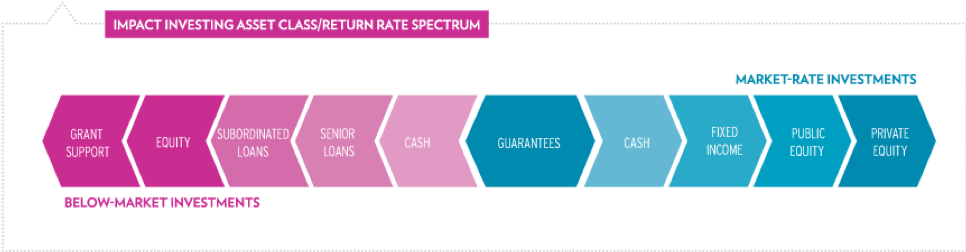

The Spectrum of Impact Investment Strategies

Impact investors aim to earn a return on their investments, but there’s a spectrum; some investors are willing to give up some of the profits if it means boosting impact.

For example, there are those who offer more favourable lending terms (ie. lower interest rates) for a business, than they might otherwise find in the market.

But the majority will expect the enterprise they invest in to offer returns that are as good, or better, than in the broader market.

In Figure 1 you can see the various asset classes that align with the returns expectations of most impact investors.

At one end you have private equity investors, they’re most likely to expect market-rate returns.

While at the other end you have grant support, which starts to look more like a charitable donation.

In between you have loans, which can be offered at variable interest rates, as well equity arrangements and guarantees.

What’s striking is that the investment options are across all asset classes. Impact investing is no longer limited to private markets.

Impact Investing in Listed Equities

There’s vigorous debate about whether you can have true ‘impact’ by investing in a company that’s listed on the stock market.

The baseline for equity investors is to consider ESG factors, but this is a ‘light-green’ approach.

When we consider Impact Investing vs ESG, we see that impact is at the more rigorous end of the spectrum. It’s good to see attempts being made to apply the high standards of impact to listed equity strategies, but there are challenges.

The key issues are;

- How can you influence the company, to steer it towards impact? It’s unlikely that you’ll have a big enough shareholding to exert your will on management.

- These companies have a dispersed roster of shareholders, as well as diverse customer base. Your focus on the broader impacts may not be shared by the other stakeholders.

- How do you measure the impact? Impact measurement is already difficult enough when shareholders and management are working together. But most big, public companies don’t yet have capacity to produce the types of data that impact investors require.

These are big challenges, but they’re not insurmountable.

If the concept of impact investing hopes to reach sufficient scale to truly shift the world towards sustainability and equality, then we’re going to have to find a way to influence these immense, publicly traded companies.

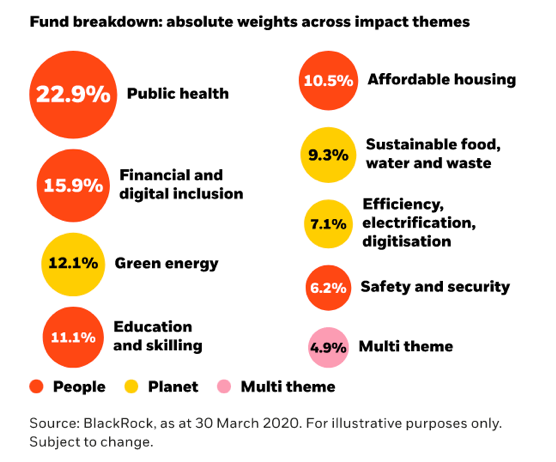

Fund managers like WHEB in the UK have a useful model that only invests in companies whose products make a positive impact.

And major fund managers like Blackrock are rolling out impact funds that track their investment’s progress in achieving the UN SDG’s.

It’s exciting that the world’s biggest fund manager is getting involved in impact investing, but, we need to ensure it’s not ‘impact-washing’.

It’s important to have clear principles about what constitutes true impact, otherwise it has the potential to dilute the good work of impact pioneers.

Blackrock received broad criticism for using the word impact to advertise funds that looked more like ESG funds. To their credit, they made changes, which resulted in the fund that’s linked above.

Some commentators remain unconvinced about the prospects for public companies to deliver impact. Paul Brest is a well-renowned academic and he sees little scope for investors to influence big companies towards positive impact.

Either way, everyone agrees that there’s one core aim here, and that is: convincing big, multinational corporations to think long-term and consider ALL of their stakeholders in their operational decisions.

Impact Investing in Fixed Income and Bonds

The fixed income asset class (mainly bonds) is well-suited to impact investing.

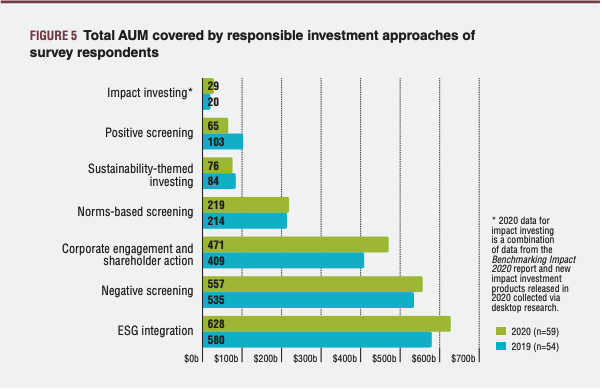

Using Australia as an example, we see a large majority of the country’s total impact investments are in the fixed-income category, mostly green-bonds.

The Responsible Investment Association of Australasia (RIAA) offers the most useful data on the state of the industry.

Their 2021 ‘Benchmark Report’ suggests that Green bond issuance makes up A$26 Billion, out of the total impact investments pool of A$29 Billion, as captured in the dataset for 2020.

I’ll go into more detail on the figures for the industry as whole in the next section, but it’s useful to note that strict impact investing makes up only 1% of the ‘responsible investment’ segment of Australia’s total Assets under Management. It’s small but highly influential.

There’s a number of reasons why fixed-income dominates the impact segment:

a) deal sizes can be scaled-up without diluting the impact, while still maintaining a small pool of large investors.

b) The structures tend to be more stable: they’re longer-term, and they’re less exposed to daily market moves. This makes it easier to capture impact data.

It makes sense for debt markets to engage with impact investing. Not only due to the risk-mitigating nature of responsible investments, but simply because they offer another layer of analysis and stability.

What are green bonds?

Green bonds were created to fund projects that have positive, environmental impacts. The mandate of a Green Bond will define both the projects that it will fund, as well as its expected impacts. This may sound subjective, and even ambiguous, but the success of green bonds has come from the rigorous accountability and regulatory frameworks built by the Climate Bonds Initiative.

This independent organisation works to set standards in the industry, to build trust around its products. And it guides research and policy, to nurture its evolution.

No self-respecting impact investor would engage with a green bond strategy that wasn’t certified by the Climate Bonds Initiative.

So successful has this sector been that’s it led the way for new debt structures like:

- Sustainability bonds

- SDG bonds

- Social impact bonds

Social impact bonds

Bonds are a difficult financial concept to explain, and social impact bonds (SIBs) are even more difficult, but they are proving to be powerful instruments, so let’s dive in.

Essentially SIBs are a way to balance risk between a government who wants to achieve an outcome, an impact investor who is willing to put capital on the line, and a service provider who is ready to get started.

It’s essentially an outcomes-based contract in which the service provider agrees to receive a portion of the payment, contingent on achievement of certain hurdles.

The pioneering example is the Peterborough Prison bond in the UK. It raised £5 million in 2010 with the goal of reducing re-offending rates by prison inmates with short sentences.

So in this situation, the key parties were:

- The local government

- Investors

- Prison rehabilitation operator

The government body stated its terms: if Peterborough’s re-conviction rates are at least 7.5% below that of a control group, then investors receive a payment that increases in proportion to the improvement in relapse rates. It was capped at 13% over 8 years.

So, instead of the government running the rehabilitation process, they incentivised the private sector to achieve the goal, hoping it would do so more efficiently.

And it worked; in 2017 the Ministry of Justice announced that re-offending rates had dropped by 9%.

The investors got their principle back, plus 3%.

Since then, the concept has gone global, and the market has done what it does best; it’s used financial incentives to motivate innovation and creativity. Here’s a few examples of creative application of the concept:

A collaboration between the NSW Government and UnitingCare Burnisde, with investment managed by SVA.

The aim was to help some of the state’s most vulnerable families to build better relationships and break a destructive cycle of abuse and neglect.

The bond raised $7 million. Four new centres were opened over the 7-year period of the bond.

BOLD – Beneficial Outcomes Linked Debt

BOLD is a funding tool developed by Impact Investment Group to fund high impact enterprises. This first iteration offers a loan to Xceptional to assist in their work empowering people with autism to utilise their unique skills, and fill roles in tech and software development.

If the loan recipient’s impact increases, then the loan decreases—it’s an outcomes-based contract.

Impact investing in Property

Impact investing is not an asset class, it’s a lens through which an investor views a particular asset, and impact investors have been eyeing-off the real estate sector for decades.

Housing and commercial property are vital to a thriving economy, it’s something we all depend on, which also means there’s a huge potential for impact.

This impact can come in many forms:

Support for social enterprise and social housing

Big Society Capital is a leading impact investor in the UK, and they know the power of offering affordable housing and commercial rents. They unite valuable skills in property investment and management, and they apply it to supporting those in need, and those building businesses that are doing good.

They invest in the Cheyne Capital Social Impact Fund, which buys property, develops homes, and then offers affordable rental terms to people that have limited options. They support people with disabilities, and they work with impact businesses to help them thrive.

They define their impact, as well as their returns. They can offer stable housing for people at risk, while also offering a stable dividend for investors who care.

Rejuvenation of old buildings

The Kensington Wool Store was built in Melbourne in 1906, and today, Impact Investment Group (IIG) is breathing new life into the space and the surrounding area.

The site was controlled by the Younghusband Company for most of last century, and it has historical significance for the Australian wool industry.

IIG aims to make it a carbon water and waste neutral site. Heating and cooling will be energy efficient, as will water management. Its impact comes from going above and beyond regulated standards of environmental awareness and social cohesion.

It’s proof, to the broader building industry, that community management and environmental excellence can be drivers of returns, and not just added costs.

High-impact new builds:

Part of the US government’s tax reforms in 2017 was an innovative approach to development called Opportunity Zones. The policy offers tax breaks for investors to sell existing assets, and then deploy the capital to build in areas that are struggling with urban development.

The Catalyst Fund has recognised the opportunity to combine their impact philosophy with favourable tax treatment. They have a housing project in Bozeman, Montana that will offer affordable rent to the population of workers who are moving to the area.

But is it additional?

There are detractors, those who say that these multimillion-dollar property developments would have happened with or without the impact title splashed on their prospectus.

This claim gets to the heart of the issue of additionality. It’s asks the question; ‘Is this project additional to mainstream investment flows?

This is core to whether they’re having genuine impact.

I’ll deal with additionality in a moment.

But first, let’s talk size.

How big is impact investing in dollar terms?

Global sustainable investment assets reached a massive US$35.3 trillion in 2020, according to the Global Sustainable Investing Alliance.

Within this US$35.3 trillion, there is US$352 billion of impact capital worldwide.

In Australia, the total pool of investment capital that’s managed with ‘responsible investment’ principles was A$1,281 billion (US$948 billion) in 2021, which represents a healthy 40% of total assets under management.

Impact Investing reached A$29 Billion (US$21 billion), in 2021.

What is ‘Additionality’ in Impact Investing?

When I first discovered the concept of impact investing there was one question I struggled with: if these investors are making market-rate returns, wouldn’t all investors be ready to deploy capital, isn’t it just regular-old-investing?

I didn’t know it at the time, but my question was about additionality. It’s about whether an investor’s impact approach is actually driving capital to an enterprise that wouldn’t otherwise have access to funds.

The writing of Paul Brest helped me greatly in my early research, and I was lucky enough to speak to him on my podcast a few years later.

Similar insights came from Andy Kuper, the founder of Leapfrog.

Both of these impact pioneers explained that the art of private equity investing was about identifying opportunities that others don’t see.

Applying an impact lens to the world, they said, opens up opportunities for purpose and profit.

Andy Kuper calls it Leapfrog’s ‘special sauce’.

While Paul Brest used the example of investors in Silicon Valley who defied the wisdom of the time to back some radical new ideas;

“If a couple of Stanford Kids came in with a poorly designed PowerPoint deck and said, ‘we have a system for indexing the web’, I would say come back when you grow up. But John Dore was smart enough to see something phenomenal, and from there comes Google.”

But of course, Google the company isn’t an impact investment, and that’s because they don’t measure their impact.

As more sophisticated structures are created, to better allocate capital to enterprises having the greatest impact, the need for accurate and verifiable impact-measurement becomes more vital than ever.

The Key Methods of Impact Measurement

Impact measurement is not subjective or ambiguous; in some cases it’s the deciding factor for the returns on a bond, and decisions around major capital allocations.

It needs to be precise, verifiable, and independent.

There are a range of frameworks available that investors use to assess the impact their investee companies are having on the world, but there remains a lack of consistency in how different groups approach the issue.

There’s no agreed global framework for how to measure impact, yet.

This makes comparison difficult across a portfolio, and it makes it difficult to verify the voracity of impact claims.

Unlike financial accounting, which has 200 years of evolution behind it, impact accounting is very new, and it still has a long way to go.

The good news is that there’s lots of work being done.

IRIS+ (GIIN)

The GIIN has developed the Impact Reporting and Investment Standards (IRIS+) which are designed to be a common reporting language for impact-related terms and metrics.

IRIS aims to enable performance comparisons and benchmarking, while also streamlining and simplifying reporting requirements for companies and their investors.

It’s the culmination of a group of 40 investors from around the world who are working to develop a standardised framework for assessing social and environmental impact.

Basically, IRIS is designed to play the role in impact investing that Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) bring to mainstream financial accounting.

Sustainable Development Goals (SDG) as Impact Framework

The SDGs are a set of 17 goals, established by the United Nations in 2015, they set the agenda for what they hope to achieve in the 15 years to 2030.

But, they’ve also become a unifying framework for companies and investors to view and measure the impacts they’re having on the world.

The power of the SDGs comes from their global scope, and its practical coverage of the 17 greatest challenges facing our world.

Companies can identify which of the goals they are achieving by shifting their products, their operations, or even just their mindset.

And, the SDGs are more sophisticated than simply a list of 17 goals.

Underneath the goals there are 169 targets which are actionable, and which allow for global comparison.

While 169 may sound like a lot, it’s actually a very broad set of targets when we consider the innumerable problems, and themes, that we need private enterprise to focus on.

Fortunately, there are a number of organisations working to integrate the SDGs into a more nuanced framework to suit specific industries, and businesses:

This tool helps companies align their strategies towards achieving the SDGs.

The online platform allows a company to enter the goals, and the sectors, that are relevant to them, and the system will suggest which indicators from other frameworks (such as the GRI) will help the company to measure, report and manage their impacts.

It was developed by GRI, the UN Global Compact and the World Business Council for Sustainable Development (WBCSD).

SDG Impact recognises the importance of impact reporting on the SDGs being verifiable and reliable. They’re aiming to remove barriers, and increase accountability.

They’re building Practice Standards that allow companies to prove that they’re actually moving the needle on the goals.

So far they’ve released a consultation draft paper on: SDG Impact Standards for Private Equity

“The Standards are designed to have value for the field as a tool to inform and help others identify effective practice that drives impact performance, create efficiencies through standardized frameworks, data management and governance structures and enable greater clarity, consistency and comparability of good practice.”

Impact Management Project (IMP)

The Impact Management Project (IMP) is a network of over 2,000 impact focussed organisations, companies and investors, working to build a consensus on how impact can be measured, benchmarked and compared.

“The work of the IMP provides a lens to understand the impact performance of different enterprises and investments against the SDGs.”

Operating Principles for Impact Management – IFC

The International Finance Corporation (IFC) has been investing for impact for more than 50 years, even if it didn’t carry that title.

The IFC is the World Bank’s private sector arm. They drive economic development by offering investment and advisory services to businesses in less-developed countries.

At the beginning of 2019 they launched the Operating Principles for Impact Management. It’s a framework to help investors design their impact management systems with discipline and transparency.

They don’t prescribe specific impact measurement tools, but instead, the nine principles get everyone on the same page to bring a level of credibility and integrity; something that’s been sorely lacking. Each year the signatory’s (currently 90) progress reports will be made public, so we can see how some of the major players are managing this evolving issue.

Social Return on Investment

Social Return on Investment (SROI) is a method of measuring non-financial factors within an enterprise. The terminology comes from accounting, where ROI relates to the financial return from an investment. SROI aims to measure the positive social impact of an investment or a program, and it’s quantified in monetary terms.

Not everyone agrees that a monetary factor is an appropriate proxy for value. But the comparison is an effective way to fit social value into standard financial accounting.

The principles and methodology were developed by Social Value UK and continue to evolve.

The end of Impact Investing

Right now, it’s only impact investors who rigorously measure their impact. The longer-term hope is that eventually, all companies will report their impact, both positive and negative.

And that way, we won’t need the term anymore, because impact will become core to the financial calculus.

Impact will sit alongside risk and return as a fundamental metric for analysing a company.

Glossary of key global institutions in the impact investment sector

The Global Impact Investing Network (GIIN) convenes the world’s leading Impact Investors to collaborate, educate and drive the evolution of the sector.

The Global Steering Group for Impact Investment (GSG) was established in 2015 to take over from the Social Impact Investment Taskforce established under the UK´s presidency of the G8.

The GSG has 32 country members. It unites business, finance and aid organisations to drive the impact movement forward.

The UN Supported-Principles for Responsible Investment (PRI) is a member-based organisation that brings together companies who are leading the charge on responsible investment.

Their membership base is broader than just impact investors, but all members agree to operate under their six investment principles.

The International Finance Corporation (IFC) is the private-sector arm of the World Bank. They’re the original Impact Investors. The IFC drives development through economic growth. It finances and advises businesses and organisations with the potential for positive impact.

This is Part 1 of the ‘Future of Investing’ series.

Part 02 is here: ESG investing vs Impact Investing vs Ethical & Sustainable; what’s the difference?

Part 03 is here: 5 ways ESG investing is changing the world of finance